In recent years, there has been a significant rise in biodiversity and nature reporting frameworks driven by various organizations.

The adoption last July of the standards related to the CSRD (Corporate Sustainability Reporting Directive) proposed by EFRAG (European Financial Reporting Advisory Group) marked an important milestone – a development resonating with the publication of voluntary frameworks TNFD (Taskforce on Nature-related Financial Disclosures) and SBT for Nature (Science-Based Targets for Nature). More recently, TNFD and EFRAG signed a cooperation agreement to clarify the interoperability of their two approaches by April 2024.

Companies and financial actors are currently trying to embrace the three frameworks: TNFD V1 was released in September after a nine-months preparatory phase, the CSRD is applicable since January 2024 and the target setting process of SBT for Nature is currently being pilot tested by more than 15 companies.

The CSRD is now mandatory for companies already subject to the Non-Financial Reporting Directive (NFRD), as well as those exceeding 500 employees, with a turnover exceeding €50 million or a balance sheet exceeding €25 million. It refers to and relies on TNFD and SBT for Nature frameworks to delve into specific subjects, particularly in its topical standards dedicated to nature related issues (ESRS E2 Pollution, ESRS E3 Water and marine resources, ESRS E4 Biodiversity and Ecosystems).

Leveraging I Care’s expertise in biodiversity metrics as well as in nature related reporting and strategies, we compared the metrics presented in the CSRD (with a focus on ESRS E4), TNFD and SBT for Nature frameworks. The choice of metrics related to nature and biodiversity is indeed a major challenge due to the inherent complexity of biodiversity and to the lack of a universally recognized metric to address this issue (unlike the kg of CO2 equivalent for climate). This comparative analysis aims at shedding light on similarities and differences that exist between frameworks, and so on the additional efforts required for a company wishing to go beyond regulatory compliance and align with the guidelines set out in voluntary frameworks aimed at fostering business model transformation (TNFD, SBT for Nature).

Overview of the Frameworks

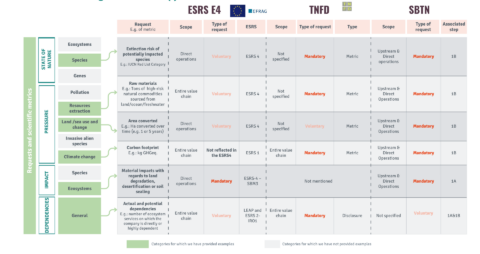

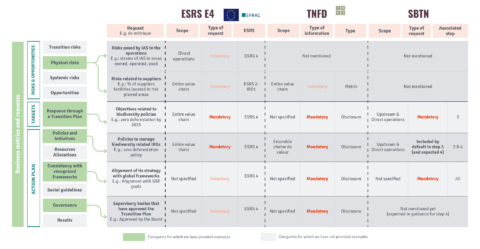

The table below summarizes the similarities and differences across frameworks from different perspectives:

In this context, it is worth noting that the CSRD and TNFD do not pursue the same goals as SBT for Nature: while the CSRD and TNFD intend to guide companies in disclosing information related to nature and biodiversity and are as such reporting frameworks, SBT for Nature is more of an engagement framework, aiming at driving transformative change. The SBT for Nature framework intends to support companies in setting “science-based targets”, alleviating pressures on biodiversity and realigning their activities and business model on ecological thresholds.

Methodological approach

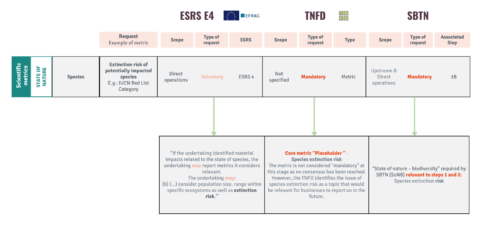

The following three figures illustrate the method we used to evaluate disparities across the metrics required under the different frameworks:

1. General approach

2. Determining whether the requests are mandatory or voluntary

3. Illustrative examples

Extracts from Our Results

Cross reading I

Cross reading II

Key Learnings

The CSRD, TNFD and SBT for Nature frameworks differ at various levels:

1. The ecological scopes covered by the frameworks vary slightly:

- Focusing on biodiversity and ecosystems for ESRS E4 and SBT for Nature, while TNFD takes a broader approach to nature.

- TNFD states that “nature refers to the natural world, emphasizing the diversity of living organisms, including humans, and their interactions with each other and with their environment” thereby including biodiversity in its approach. In practice, this scope distinction has a moderate impact on the mentioned metrics.

2. The topics addressed differ as well:

- TNFD particularly emphasizes the identification of risks and opportunities related to nature, governance, and the company’s impacts on indigenous populations and local communities.

- The CSRD addresses subjects related to indigenous populations and local communities in detail in other standards other than ESRS E4, namely ESRS E2 General Disclosures, ESRS G1 Business Conduct, and ESRS S3 Affected Communities. It also addresses risks, albeit demanding fewer specific metrics than TNFD on the subject, asking, for example, for companies to assess their physical, transition, and systemic risks.

- The SBT for Nature framework – which focuses on impacts and their reduction – addresses the issue of local and indigenous populations in an optional step and does not explicitly mention governance or risks as such.

3. The application scope of metrics differs across the three frameworks:

- SBT for Nature systematically covers upstream value chain and direct operations, thus offering a more comprehensive view, while the other two frameworks present a less extensive scope, mostly focused on direct operations.

- For most metrics, the CSRD and TNFD let companies determine the scope of their reporting based on a materiality self-assessment.

4. The frameworks differ in their approach to metrics:

- While SBT for Nature focuses on pressures and the state of nature to define targets, standing out for its stringent requirements regarding a.o. geographical data, TNFD and the CSRD are less specific.

- For instance, SBT for Nature details land use changes by locality and type of use, across direct operations and the upstream value chain, while they are aggregated in the CSRD and mandatory only for direct operations. It is important to note, however, that the CSRD ideally encourages companies to publish this information across their entire value chain.

- The CSRD, ESRS 4 covers an extensive range of metrics related to business conduct. It requires the publication of changes made in ecosystem management and, if applicable, key performance metrics about the offsets that are part of biodiversity and ecosystems-related actions.

- TNFD, on the other hand, suggests a wide range of risk-related metrics. The framework asks companies to provide numerous financial metrics related to risks, such as exposure to increased operational costs or revenue loss due to reputation-related risks.

5. Despite their differences, these three frameworks are closely interconnected, and complement each other coherently:

- By fulfilling CRSD requirements on biodiversity under ESRS 4 (if biodiversity is deemed a material topic) companies match TNFD’s recommendations quite well on the specific theme of biodiversity but not on wider nature-related issues. As TNFD focuses on nature in a broader sense, some of its recommendations are indeed not covered by ESRS E4. Regarding the CSRD, it refers to TNFD by recommending the LEAP approach as a tool for companies to carry out the materiality self-assessment of biodiversity-related topics.At last, SBT for Nature is mentioned by both the CSRD and TNFD: the CSRD recommends that companies referring to ecological thresholds to set targets base on the guidance provided by SBT for Nature, to make sure that the above-mentioned targets are science-based. Regarding TNFD the framework refers to SBT for Nature on several occasions, be it for identifying high-risk natural commodities (SBT for Nature’s HICL list) or when it comes to actions to be implemented to respond to nature-related risks and opportunities (mitigation hierarchy, conceptualized through SBT for Nature’s AR3T framework)

- However, complying with CSRD requirements and TNFD recommendations constitutes only a preliminary step in the SBT for Nature process. The latter goes further by offering a science-based approach for the company to set targets aligned with ecological thresholds while also taking into account the UN sustainable development goals, with the aim to drive a profound transformation of practices across both value chains and direct operations. In this sense, SBT for Nature is characterized by a more strategic, as well as a more practical edge.

Although the frameworks are closely intertwined and while the work carried out to comply with one of them supports compliance with the other two, they reflect varying degrees of ambition across companies adopting them.

To sum up

Meeting the CSRD requirements is a matter of regulatory compliance. While the final version of the CSRD introduces a greater level of flexibility compared to the first drafts, it provides a demanding foundation for disclosure on biodiversity issues: it requires the disclosure of a broad range of qualitative and quantitative information, while giving some latitude regarding the choice of metrics.

TNFD, a framework cited by the CSRD, helps companies navigate the path towards regulatory compliance: this framework provides indeed companies with a robust methodology to use to report on and address their nature issues – even though the framework goes beyond the CSRD requirements on a number of subjects (governance, social issues, risk and opportunity analysis, among others). The TNFD framework is well suited for financial actors that are ambitious in the way they manage their investment portfolios.

Targeting in essence companies willing to engage in ambitious environmental policies, the SBT for Nature framework stands out with its high level of precision, notably because it requires extensive data collection and detailed analysis of pressures upstream in the company’s value chain. In this sense, SBT for Nature requires companies willing to go through its steps to invest extra effort, attention, and time. At the same time, SBT for Nature constitutes a real opportunity for embarking on a transformation journey towards a more “resilient” business model, in line with “planetary boundaries” – a journey that the CSRD calls for as well, even if under the final version of the Directive, the disclosure of a “transition plan” is not mandatory anymore in relation to biodiversity. In this sense, the spirit of the European regulation is quite in line with the letter of the SBT for Nature framework: from that standpoint, SBT for Nature provides a robust framework for companies to get familiar with new and complex concepts and put their business model to the test of major environmental challenges.

Taking Action

I Care by BearingPoint assists its clients in interpreting and implementing the CSRD based on a rigorous understanding and ambitious operationalization of the legislation.

This approach aims at helping our clients avoid reputational risk and turn compliance to a competitive advantage, in the context of a constantly evolving regulatory landscape. The team also aims at supporting all players willing to embrace the TNFD framework or to embark on a SBT for Nature journey (Steps 1, 2 and 3), which has become an essential catalyst for transitioning towards more sustainable, resilient and “nature-positive” business models.

Find all of our latest publications in the Infos tab of our website